Your personal car insurance policy likely leaves a massive hole in your coverage the moment you climb into a 26-foot box truck. Most standard policies and credit cards explicitly exclude vehicles over a specific weight. This leaves you fully liable for every scratch or dent. Understanding your moving truck rental insurance options is the only way to bridge this gap. You shouldn’t have to guess while a clerk pressures you at the rental counter. We know the alphabet soup of PDW, SLI, and PAI feels like a calculated attempt to drain your wallet. It’s frustrating to face hidden liabilities when you’re already stressed about moving your entire life.

You deserve to master these protections so you can choose the right coverage without overpaying. This 2026 comparison guide breaks down the latest offerings from major providers like U-Haul, Penske, and Budget. We provide a clear “yes/no” framework for each insurance type. You’ll gain the confidence to spot a scam and the data to secure the lowest total cost for your journey. We’ve stripped away the industry jargon to give you the facts you need for a friction-free experience. Let’s get your belongings protected without the fluff.

Key Takeaways

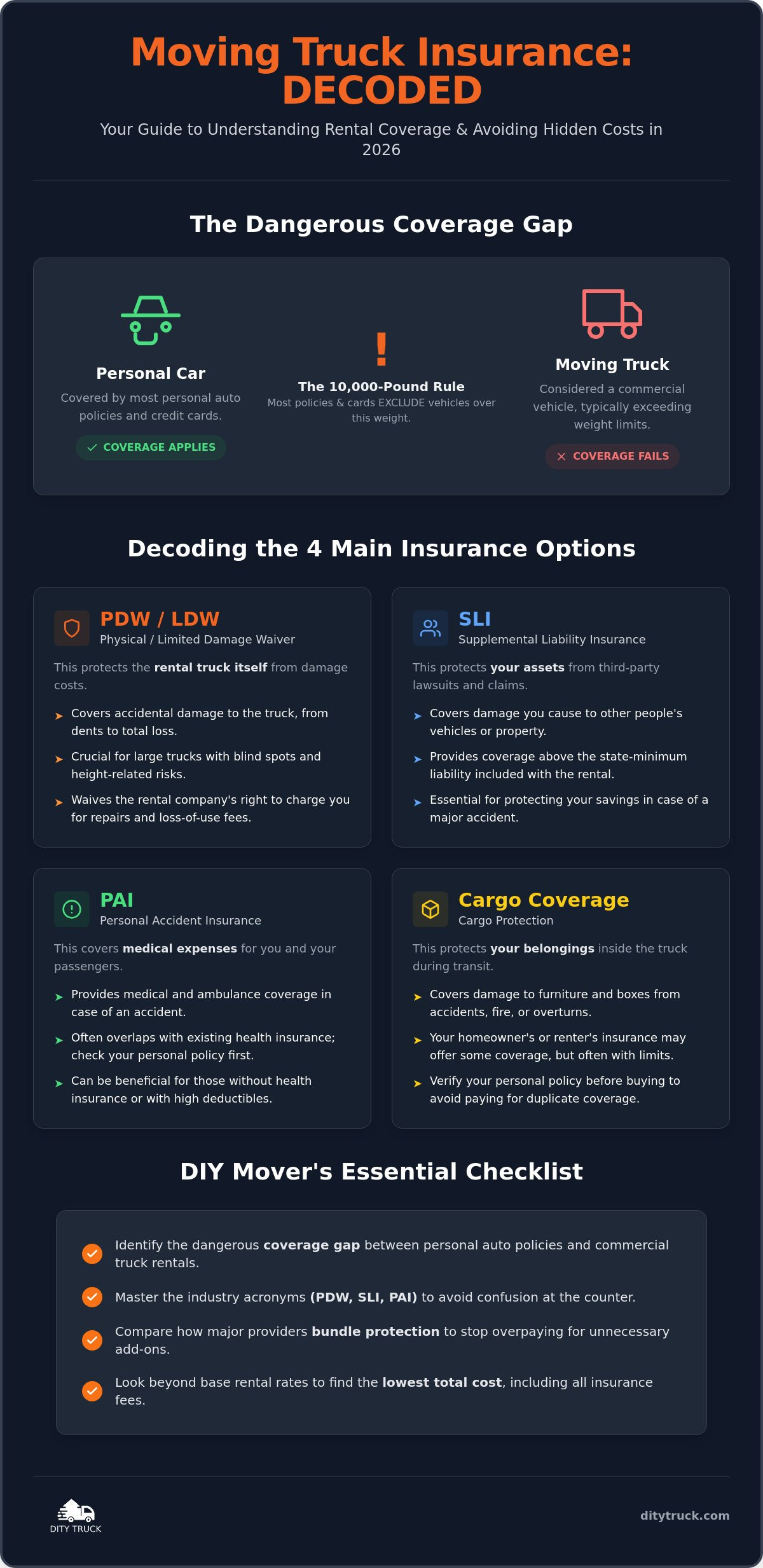

- Identify the dangerous gap between personal auto policies and commercial truck rentals.

- Master the industry acronyms for moving truck rental insurance options. Avoid confusion at the counter.

- Compare how major providers bundle their protection products. Stop overpaying for unnecessary add-ons.

- Use our simple framework to determine which insurance types are essential for your move.

- Look beyond base rates to find the lowest total cost. Insurance fees often change which truck is actually cheapest.

Why Your Personal Car Insurance Likely Fails with a Moving Truck Rental

Don’t assume your current car insurance follows you into the cab of a box truck. It’s a common mistake that leads to massive financial liability. Most personal auto policies are written specifically for passenger vehicles. They aren’t designed to cover a 15,000-pound machine. This creates a dangerous insurance gap. You might think you’re covered, but the fine print usually says otherwise. Exploring moving truck rental insurance options isn’t just an extra cost. It’s a necessity because your existing policy likely stops at the bumper of your SUV.

A 26-foot box truck is legally classified as a Commercial vehicle. It handles differently, requires more braking distance, and causes significantly more damage in an accident. Because of these risks, insurance companies draw a hard line. Standard U.S. auto policies typically contain a weight exclusion clause that denies coverage for any vehicle with a Gross Vehicle Weight Rating (GVWR) over 10,000 pounds.

The 10,000-Pound Rule and Your Credit Card

Your premium credit card likely offers rental car protection, but it has strict limits. Most cards cut off coverage at the 10,000-pound mark. A standard 10-foot rental truck often hovers right at this limit. Anything larger, like a 16-foot or 26-foot truck, is almost certainly excluded from these benefits. These cards also exclude vehicles designed for commercial use. If the truck has a ramp or a roll-up door, your card provider probably views it as a business tool rather than a personal transport.

To verify this, call the number on the back of your card. Ask specifically: “Does my rental collision damage waiver cover a vehicle with a GVWR over 10,000 pounds?” Don’t accept a general “yes” about rental cars. You need confirmation for large trucks. This simple call can save you thousands in rejected claims and provide instant clarity before you reach the rental counter.

The Risk of Out-of-Pocket Liability

If you decline moving truck rental insurance options and have an accident, you are on the hook for more than just repairs. A new box truck is a major investment for the rental company. Your personal policy limits might not even cover a total loss if the truck is destroyed. Then there are loss of use fees. Rental companies charge you for every day the truck is in the shop and cannot be rented to another customer. These daily fees add up fast. They can easily exceed the cost of the actual repairs.

Your personal comprehensive and collision coverage is built for your car’s value and risk profile. It doesn’t account for the height of a truck. Overhead damage, such as hitting a low bridge or a tree limb, is a frequent rental accident. Most personal policies won’t touch that claim because they consider it avoidable negligence. You’re left paying the full bill out of your own pocket. Buying the right protection at the counter turns a potential disaster into a minor inconvenience.

Decoding the 4 Main Moving Truck Rental Insurance Options

Understanding moving truck rental insurance options shouldn’t feel like a trap. These products exist to cap your financial exposure. They turn a potential five-figure disaster into a manageable daily fee. Most companies use a standard set of acronyms to describe their plans. Knowing them helps you stay in control when you’re standing at the rental counter. You can separate these options into two simple categories: protecting the truck and protecting yourself. Here are the four primary types you’ll encounter:

- PDW/LDW: Protects the rental truck itself from damage costs.

- SLI: Protects your assets from lawsuits and third-party claims.

- PAI: Covers medical expenses for you and your passengers.

- Cargo: Covers your furniture and boxes during transit.

Physical Damage Waiver (PDW) / Limited Damage Waiver (LDW)

A Physical Damage Waiver is your first line of defense. It isn’t technically insurance. It’s a legal agreement where the rental company waives its right to collect repair costs from you. Full waivers typically offer $0 deductible protection. Limited Damage Waivers are different. They might leave you responsible for the first $500 or $1,000 of damage. This is often the most critical coverage for DIY movers. Box trucks have massive blind spots. Scuffing a side panel or hitting a low-hanging branch is easy to do. Without a waiver, you pay the full repair bill plus fees while the truck is out of service.

Supplemental Liability Insurance (SLI)

Supplemental Liability Insurance protects you from other people’s claims. Rental trucks carry the minimum liability required by state law. These limits are often surprisingly low. If you cause an accident involving multiple vehicles, those state minimums disappear instantly. SLI fills the gap. It typically provides up to $1,000,000 in protection for bodily injury and property damage claims. This regulatory framework is outlined in this official government document. It keeps your personal savings safe if a major accident occurs on the road.

Personal Accident & Cargo Protection

Personal Accident Insurance (PAI) focuses on people. It provides medical and accidental death coverage for you and your passengers. Cargo Insurance covers your belongings while they are inside the truck. Read the fine print carefully. Cargo protection often excludes theft. It usually only covers damage from accidents, fires, or natural disasters. Some homeowners or renters policies already cover your items during a move. Check your existing policy to avoid paying twice for the same protection. If you’re looking for the best value, compare truck rental options to see how these fees impact your total move cost.

Comparing Coverage Bundles Across Major Rental Providers

Rental companies rarely sell protection like a grocery store. You can’t usually grab a small amount of cargo coverage and leave the rest behind. Instead, providers stack their products into pre-set bundles. This strategy simplifies the decision for the company but can lead to overpaying if you aren’t careful. Understanding how companies group these moving truck rental insurance options is the only way to find the best value. You must look past the base rental price to see the total protection cost. The “cheapest” truck often becomes the most expensive once you add the mandatory protection stack.

When you evaluate u-haul vs budget truck rental, you are comparing two very different protection philosophies. One company might prioritize low entry prices with high deductibles. Another might offer a higher flat rate for total peace of mind. Your goal is to find the bundle that matches your specific risk tolerance. Don’t let the clerk at the counter rush you into a “Premier” plan if a “Basic” plan covers your actual needs.

Penske vs. Budget vs. U-Haul: Protection Philosophy

Penske uses a multi-tier approach. They offer Basic, Standard, Value, and Premier levels. This tiered system allows you to scale your protection based on the distance of your move and the value of your items. Budget takes a more binary path. They typically offer “Complete Protection” or “Choice Protection” packages. Their “Complete” option often bundles a Physical Damage Waiver with supplemental liability and cargo protection. It’s a “one and done” solution for those who want zero risk.

U-Haul keeps their offerings streamlined with Safemove and Safemove Plus. Safemove is the standard choice. It covers the truck, your cargo, and medical costs for occupants. Safemove Plus is the premium upgrade. It adds a crucial $1,000,000 supplemental liability layer and covers overhead damage. This distinction is vital. Most standard plans exclude damage to the top of the truck. If you hit a low tree branch, only the premium bundle saves you from a massive repair bill.

Roadside Safety Net: Is it Insurance or a Service?

Roadside assistance is frequently sold as an insurance add-on. It functions more like a service contract than a traditional policy. For a small daily fee, you get a guarantee of help if things go wrong. This is essential for long-distance, one-way moves. You don’t want to be stranded on a remote highway with a 26-foot truck and no plan. Most bundles include this, but some companies offer it as a standalone option like U-Haul’s SafeTrip.

These service plans typically cover the most common logistical headaches. You get help with flat tires, jump-starts, and fuel delivery if you run dry. They also handle lockouts, which are surprisingly common during the chaos of loading a truck. Paying for this service upfront is a smart hedge against the high cost of private towing. A single service call for a commercial-sized vehicle can cost hundreds of dollars if you pay out of pocket.

The DIY Mover’s Checklist: Which Insurance Options Are Actually Worth It?

Most renters skip protection because they’ve never had an accident. This logic is a dangerous trap. Driving a 15,000-pound box truck is not the same as driving your daily sedan. The risk profile shifts the moment you climb into that high-back seat. Your choice of moving truck rental insurance options should depend on the complexity of your route and the vehicle size. Larger trucks carry significantly higher financial risks. They have larger blind spots and require much longer stopping distances. Total move costs are influenced by both base rates and protection plans. Check our guide on box truck rental prices to see how different sizes impact your budget.

When to ALWAYS Buy the Damage Waiver

Always buy the Physical Damage Waiver if you are driving an unfamiliar vehicle size. If you usually drive a compact car, a 26-foot truck will feel like a ship. Long-distance routes also increase your risk. Fatigue and unfamiliar highways are a recipe for minor accidents. Tight city streets are another red flag. Navigating narrow alleys or low-clearance bridges in a massive truck is stressful. The peace of mind value often outweighs the daily cost. For a first-time 26-foot truck renter, this waiver is your most important safety net. It ensures a single mistake doesn’t ruin your financial health.

When You Might Safely Skip Supplemental Coverage

You might safely skip supplemental medical or cargo coverage if your existing policies are robust. Check your health insurance first. If it covers you regardless of the vehicle you’re in, PAI might be redundant. Similarly, some high-end homeowners or renters policies cover belongings during a move. This is a form of self-insurance. It works best for those with a high net worth who can handle a deductible. However, never skip liability coverage if you are moving across state lines. Legal requirements and accident costs vary wildly between states. You need that $1,000,000 buffer to protect your assets from out-of-state lawsuits.

The “Pre-Drive” Inspection: Protecting Your Protection

The walk-around inspection is the most important part of the insurance process. Don’t let the rental agent rush you. Take time-stamped photos of every side of the truck before leaving the lot. Focus on the roof, the corners, and the tires. If you see a scratch, report it immediately. Ensure the agent marks it on the digital or paper contract. This prevents the company from blaming you for pre-existing damage when you return the vehicle. Your photos are your evidence. They protect your protection plan from being used to cover old repairs. Before you sign the contract, compare rental rates and protection plans to ensure you’re getting the best all-in value.

How to Compare Total Rental Costs and Protection with DityTruck

A low base rate is often a decoy. The cheapest truck on the screen isn’t always the cheapest at the checkout counter. Rental companies use different pricing models for their protection plans. One provider might offer a rock-bottom daily rate but charge a premium for their Physical Damage Waiver. Another might have a higher base price that includes better value for their moving truck rental insurance options. Finding the true bottom line requires looking at the total package. You need to combine the base rate, estimated mileage, and your chosen protection level to see the actual cost of your move.

Chasing individual quotes across multiple websites is a waste of your time. It leads to confusion and missed details. You shouldn’t have to build a spreadsheet just to move your furniture. This is where a streamlined comparison becomes your most valuable tool. By looking at the all-in value, you avoid the high-pressure sales tactics at the rental counter. You arrive at the lot knowing exactly what you’ll pay and exactly what is covered.

Transparent Comparison for Smarter Booking

DityTruck acts as your smart assistant by aggregating data from major providers. We show you real-time availability and pricing in one clean interface. Comparing moving truck rental options in one place saves hours of tedious research. You can see how a Penske bundle stacks up against a Budget plan before you ever click “Reserve.” This transparency strips away the complexity of logistics. It replaces stress with confident simplicity.

Our platform highlights the distinctions in protection philosophy we discussed earlier. You can quickly spot which bundles include roadside assistance or zero-deductible waivers. Seeing these details side-by-side allows you to make a savvy consumer choice. You aren’t just booking a truck. You are securing a friction-free solution for a high-stakes task. This clarity ensures you don’t overpay for coverage you don’t need or leave yourself exposed to hidden liabilities.

Final Steps: Booking Your Protected Move

Your path to a stress-free move is a simple, logical progression. Start by entering your dates and locations. Compare the total rates that include your preferred protection tier. Select the truck that fits your volume and your budget. Add your moving truck rental insurance options with a single click. This methodical approach prevents you from feeling overwhelmed. You move with the confidence that your belongings and your bank account are safe.

We perform the heavy lifting behind the scenes so you don’t have to. DityTruck simplifies the logistics. You focus on the packing and the new house. There is no unnecessary preamble in our process. It is the shortest, most logical path between your current problem and a successful resolution. Stop guessing and start knowing. Find and compare your moving truck rental today and take the first step toward a confident, protected move.

Secure Your Move with Confidence

Don’t let the complexity of logistics slow you down. You now have the tools to identify the dangerous gaps in your personal auto policy and navigate industry acronyms like a pro. Choosing the right moving truck rental insurance options isn’t about spending more. It’s about protecting your assets and your peace of mind. Remember to prioritize the physical damage waiver for large trucks and always perform a detailed pre-drive inspection. By focusing on the total all-in cost, you ensure that hidden fees don’t derail your moving budget.

DityTruck simplifies this process by providing real-time rate comparisons from major national providers. Our platform is designed for DIY movers who value transparency and efficiency. There are no hidden platform fees. We provide clear data to help you make the best choice for your journey. Compare moving truck rates and protection options in seconds. You’ve done the research. Now, take the final step toward a friction-free move. Your belongings are ready, and now your protection plan is too. Safe travels to your new home.

Frequently Asked Questions

Does my personal car insurance cover a moving truck rental?

Your personal auto policy likely excludes any vehicle over a specific weight limit. Most standard policies stop coverage at 10,000 pounds Gross Vehicle Weight. This means a 15-foot or 26-foot box truck is strictly out of bounds. You should call your agent to confirm. However, relying on personal insurance for these larger vehicles is a high-risk gamble that usually results in a denied claim.

Will my credit card cover damage to a rental box truck?

Credit card rental benefits almost never apply to box trucks or cargo vans. These benefits are designed for passenger cars and SUVs. Cards specifically exclude commercial-grade vehicles and trucks with more than four wheels. If you rely on your card’s secondary insurance, you will likely face the full repair bill yourself. Always check your benefits guide for the “truck and van” exclusion clause before you decline other moving truck rental insurance options.

What is the difference between LDW and PDW in truck rentals?

The main difference lies in your out-of-pocket responsibility. A Physical Damage Waiver (PDW) typically offers a $0 deductible. It covers the full cost of truck repairs. A Limited Damage Waiver (LDW) might leave you responsible for the first $500 or $1,000 of the damage. Both are contractual agreements where the company waives its right to collect from you. Check the specific terms of your rental to see which waiver they offer.

Is cargo insurance worth it for a local move?

Cargo insurance is often worth the small daily fee even for short distances. Local moves still involve risks like sudden stops, shifting furniture, or vehicle fires. While your homeowners policy might cover some items, it often has a high deductible. Rental cargo insurance provides a lower barrier to reimbursement. It ensures your couch and electronics are protected from transit accidents without risking your primary insurance rates.

What happens if I get into an accident in a rental truck without insurance?

You become personally responsible for all financial losses. This includes the cost to repair or replace the truck. You also pay “loss of use” fees for every day the truck is out of service. If you injured someone else, you could face massive third-party liability claims. Without the protection of moving truck rental insurance options, these costs can easily lead to long-term debt or legal judgments.

Can I buy moving truck insurance from a third party instead of the rental company?

Third-party options exist but are not common for one-day rentals. Some companies offer specialty moving coverage or annual non-owner policies. However, these are often more complex to set up than simply buying the rental company’s plan. Most renters choose the convenience of the counter-offered protection. It is already vetted to match that specific fleet and provides immediate, on-site claim handling if something goes wrong.

Does U-Haul insurance cover the car I am towing on a trailer?

U-Haul’s Safemove and Safemove Plus focus on the rental truck and its cargo. They do not automatically cover a personal car being towed on a trailer. You must add Safetow protection to cover damage to your own vehicle during transit. This specific add-on covers the towed car against collision and theft while it is attached to the rental truck. Always verify that your personal car is listed on the protection contract.

Is roadside assistance included for free with moving truck rentals?

Basic mechanical assistance for engine failure is usually included in the base rate. However, convenience roadside assistance is often a paid extra. This covers issues like locking your keys in the cab, jump-starts, or running out of gas. If you don’t pay for the supplemental roadside plan, you will be billed for the service call. These fees are significantly higher than the small daily price of the protection add-on.

Leave a Reply