Did you know that your “full coverage” auto insurance probably treats a 15-foot moving truck like a piece of heavy commercial machinery rather than a personal car? Most people wait until they’re standing at the rental counter to ask, do I need insurance for a rental truck, only to face a high-pressure sales pitch and confusing jargon. It’s a stressful moment that often leads to expensive mistakes. You’re right to be skeptical of the upsell, but you’re also right to worry about the massive financial risk of driving a vehicle that’s significantly larger and heavier than your daily driver.

We’re here to strip away the complexity and give you a straight answer. We agree that you shouldn’t have to pay twice for the same coverage, but you also can’t afford to leave your savings unprotected. You’ll learn exactly where your personal policy and credit card coverage fall short, especially since most major providers exclude large moving vehicles in 2026. We’ll break down the specific costs for supplemental liability options and damage waivers so you can spot a fair deal. This guide identifies the gaps in your current protection and helps you find the cheapest total rental package for your move.

Key Takeaways

- Most personal auto policies and credit cards exclude vehicles over 10,000 pounds. This leaves you fully liable for a standard moving truck unless you secure specific coverage.

- To answer “do I need insurance for a rental truck,” look for cargo exclusions in your current policy. Standard insurance usually ignores the items inside the truck.

- Learn to distinguish between Damage Waivers that cover the truck and Supplemental Liability Insurance that protects you against third-party claims.

- Use our five-step checklist to verify coverage with your agent. This prevents double-paying for protection you might already have through homeowners or renters insurance.

- Focus on finding the lowest base rental rate first. This strategy frees up your budget to afford the comprehensive protection required for a stress-free move.

Do You Need Insurance for a Rental Truck? The Quick Answer

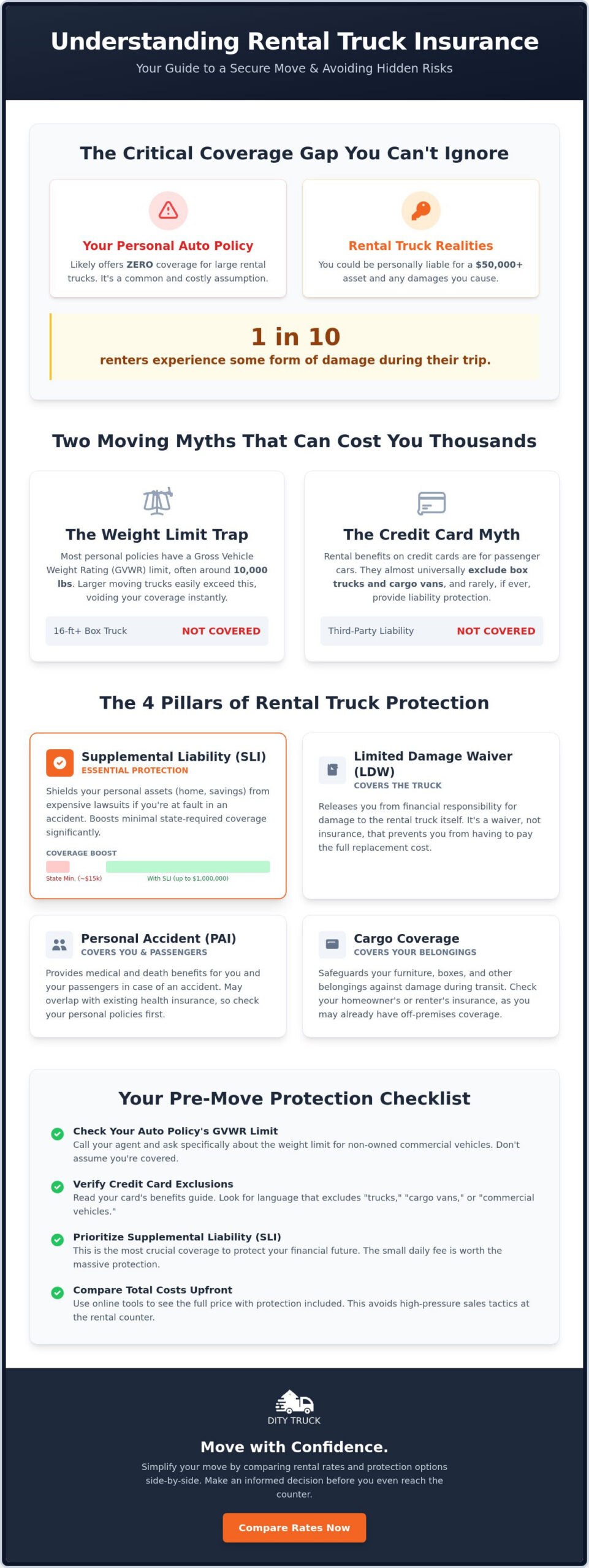

If you are asking yourself, do I need insurance for a rental truck while standing at the rental counter, the short answer is almost always yes. Most personal auto policies are designed for standard passenger cars and SUVs. They typically exclude cargo vehicles and trucks used for moving. This gap in coverage leaves you personally responsible for every dollar of damage if an accident happens. Relying on your daily driver’s policy is a high-stakes gamble that rarely pays off for DIY movers.

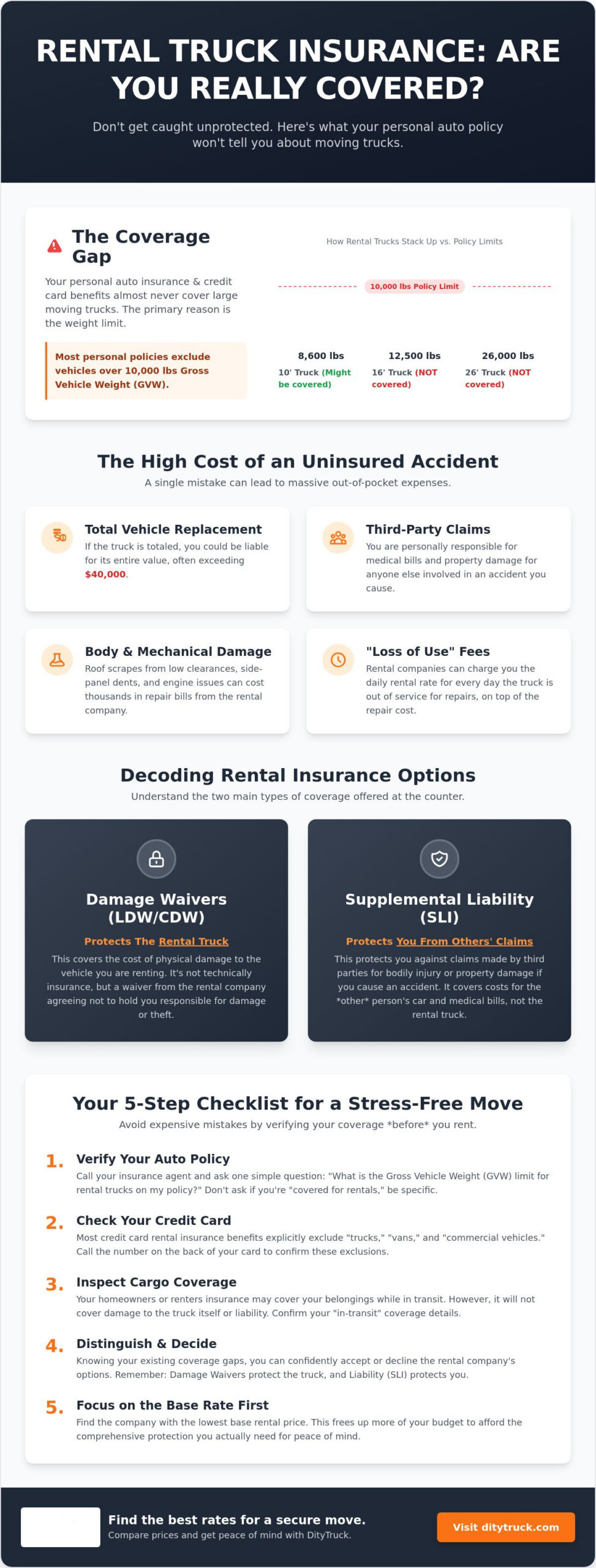

Size is the primary factor in this coverage gap. Most personal insurance providers draw a hard line at 10,000 pounds Gross Vehicle Weight (GVW). If your rental truck exceeds this weight limit, your standard policy likely provides zero protection. Since even a modest 10-foot or 15-foot box truck often hits this threshold when fully loaded, you are essentially driving without a safety net. You face two distinct financial risks: liability for damage caused to others and physical damage to the truck itself.

The Definition of a Rental Truck in Insurance Terms

Insurers view a 10-foot box truck differently than a large SUV because of the risk profile. Passenger vehicles are built for people. Commercial-use trucks are built for freight and require different handling. Understanding Vehicle Insurance Basics helps clarify why these categories don’t mix. GVW represents the maximum operating weight of a vehicle including its load, and reaching this limit is often the exact point where personal insurance coverage ends. Your policy likely lists these exclusions in the fine print under “commercial” or “cargo” vehicle definitions.

The High Cost of Being Uninsured

Mistakes behind the wheel of a large truck are expensive. A simple scrape against a low-hanging tree branch or a dent from a tight parking maneuver can cost thousands of dollars in bodywork. Rental companies also charge “Loss of Use” fees. You pay the daily rental rate for every day the truck is in the shop and unavailable for other customers. In a total loss scenario, you could be held liable for the entire replacement cost of the vehicle, which often exceeds $40,000. These costs can quickly eclipse the price of a protection plan. When you wonder, do I need insurance for a rental truck, consider these potential out-of-pocket expenses:

- Mechanical damage: Transmission or engine issues caused by improper towing or overloading.

- Body damage: Roof scrapes from low clearances or side-panel dents.

- Third-party claims: Medical bills or property damage for other drivers involved in a collision.

- Administrative fees: Processing costs and appraisal fees charged by the rental company after an accident.

Why Your Personal Auto Policy and Credit Card Often Fall Short

Assuming your existing coverage follows you into any rented vehicle is a dangerous mistake. When you ask, do I need insurance for a rental truck, the answer lies in the fine print of your current agreements. Personal auto policies are written specifically for passenger vehicles. They include restrictive language that excludes “commercial-style” or “cargo” vehicles. If you cause an accident in a vehicle that exceeds your policy weight limit, your insurer can legally deny the claim. This leaves you personally responsible for medical bills, property damage, and the cost of the truck itself.

Weight Limits and Your Policy Fine Print

You can find your specific restrictions by checking the Declarations Page of your insurance policy. Most personal providers cap coverage at a Gross Vehicle Weight (GVW) of 9,000 to 10,000 pounds. This figure represents the total weight of the truck combined with its maximum cargo capacity. It’s not just about how much the truck weighs while empty. It’s about what it is capable of carrying.

- 10-foot trucks: These often sit around 8,600 lbs GVW and might be covered by some premium policies.

- 16-foot trucks: These typically jump to 12,500 lbs GVW, which is well beyond standard personal limits.

- 26-foot trucks: These heavy-duty vehicles can reach 26,000 lbs GVW.

A small pickup truck rental is usually the only exception to this rule. Anything with a box or a cargo shell is viewed as a different class of risk by your insurer. You should look for the GVW sticker on the driver’s side door jamb of the truck to verify its rating before you drive off the lot.

The Credit Card Insurance Myth

Relying on a credit card for protection is a common trap for DIY movers. Most major cards from Visa, Mastercard, and American Express explicitly exclude “trucks,” “cargo vans,” and “vehicles with a bed” from their rental benefits. Even if you rent a small cargo van that feels like a standard SUV, the commercial classification on the registration usually triggers an exclusion. You should carefully review how a collision damage waiver functions before assuming your card provides any safety net.

These card benefits are also typically “secondary” coverage. They only pay out after your primary insurance has been exhausted. If your primary auto insurance denies the claim because the truck is too heavy, the secondary card coverage often won’t kick in at all. This creates a total gap in protection. Before you commit to a vehicle, it’s a good idea to compare rental truck rates that offer clear, upfront protection packages to avoid these hidden gaps.

Finally, consider the “Cargo Exclusion.” Even if your policy covers the truck, it almost certainly won’t cover the contents. If a fire or theft occurs, your personal auto policy provides zero reimbursement for your furniture or electronics. Moving for business purposes further complicates things. If you are transporting office equipment or inventory, a personal policy is immediately voided in the eyes of most insurers.

Breaking Down Rental Truck Insurance Options: What’s Actually Covered?

Understanding your options at the counter is the only way to avoid overpaying. You already know your personal policy likely has gaps. Now you need to decide which specific protections close them. When you ask, do I need insurance for a rental truck, you are usually looking for a combination of these four core products:

- Damage Waivers: Releasing you from financial responsibility for the truck.

- Supplemental Liability: Protecting you against claims from other people.

- Cargo Protection: Covering your furniture and personal belongings.

- Personal Accident: Handling medical costs for you and your passengers.

Damage Waivers: The Most Important Add-on

A Collision Damage Waiver (CDW) or Loss Damage Waiver (LDW) is the foundation of moving protection. A waiver is a contractual agreement, not a policy. It means the rental company agrees not to hold you financially responsible for damage to their truck. Full coverage waivers typically have a zero deductible. This means you can walk away from a totaled vehicle without paying a cent. Limited versions might only cover certain types of damage or include a high deductible. This is the most common protection chosen by DIY movers because it eliminates the risk of paying for a $40,000 replacement vehicle out of pocket.

Supplemental Liability Insurance (SLI) protects your bank account from third-party claims. If you hit another car or damage a building, SLI covers the injuries or property damage you caused to others. Standard rental agreements often include only the bare minimum state liability, which is rarely enough for a major accident. In 2026, premium supplemental plans offer up to $1,000,000 in additional coverage. Other providers might cap this at $750,000 to meet federal requirements for interstate carriers. This is vital because a 20,000-pound truck can cause massive damage in seconds compared to a standard car.

Cargo and Life Protection

Your belongings are often the most overlooked part of the move. Homeowners or renters insurance might cover your furniture while it is in your house, but coverage often stops once the items are on the road. Cargo protection covers your goods against specific risks like fire, windstorms, or the truck overturning. Most plans have strict exclusions. For example, damage from shifting loads or theft from an unlocked truck is rarely covered. You should check the limits for water damage specifically. Leaky roof seals are a common issue in older rental fleets. Personal Accident Insurance (PAI) is often bundled here to help with medical bills for you and your passengers if an injury occurs during the trip.

Don’t ignore the value of 24/7 Roadside Assistance. It covers lockouts, jump-starts, and tire changes. Without it, a flat tire in a remote area can cost you hundreds of dollars in towing fees and hours of lost time. Choosing a comprehensive package often provides the best value and the most peace of mind for a long-distance haul.

5 Steps to Verify Your Coverage Before You Rent

Confirming your protection before you reach the rental counter saves time and prevents expensive double-payments. Many movers assume they are covered only to find out their policy has a hidden weight limit. You can solve the mystery of do I need insurance for a rental truck by following these five logical steps. This process ensures you have a clear paper trail and complete confidence before you start the engine.

The Agent Script: What to Ask Your Insurance Provider

Your first step is a direct conversation with your auto insurance agent. Don’t settle for a vague “you should be fine” answer. Ask for specific confirmation regarding “Non-Owned Auto” coverage extensions. You need to know if your policy applies to vehicles used for moving personal property. Use these exact questions to get the clarity you need:

- “Does my current policy cover a rental vehicle with a 14,500 Gross Vehicle Weight (GVW)?”

- “Are there any exclusions for ‘cargo vehicles’ or ‘box trucks’ in my plan?”

- “Will my liability limits remain the same when driving a larger vehicle?”

- “Can you provide a written confirmation of this coverage via email?”

Once you have the answer from your auto agent, check your homeowners or renters insurance. Look specifically for “off-premises” property coverage. This part of your policy often protects your belongings while they are in transit, even if they aren’t in your home. It acts as a secondary safety net for your furniture and electronics. Before you commit to a specific vehicle, it’s helpful to review a Moving Truck Rental: The Complete 2026 Comparison & Booking Guide to see which trucks fit your verified coverage limits.

The third step involves your credit card. Download the specific “Benefits Guide” for the card you plan to use for the rental. Look for the “Rental Loss and Damage” section. If it excludes trucks or vehicles with more than four wheels, you know you cannot rely on the card for protection. Next, compare the rental company’s protection tiers. In 2026, standard damage waivers often range from $14 to $30 per day, while supplemental liability can add another $25. Compare these costs against the potential risk of a denied claim. Before you sign the contract, compare truck rental quotes to see which companies offer the most transparent protection pricing.

Pre-Rental Inspection: Your First Line of Defense

Your final step happens on the lot. Documentation is your best insurance policy. Use your phone to take a slow, 360-degree video of the truck before you move it an inch. Point out every existing scratch or dent to the rental agent. Pay close attention to the roof. Overhead damage is the most common “uncovered” area in standard protection plans. If you hit a low bridge or a tree branch, you are often responsible for the full repair cost regardless of the waiver you purchased. Checking the roof for pre-existing scrapes protects you from being blamed for someone else’s mistake. This simple walkthrough turns a high-stakes gamble into a managed, professional move.

Balancing Insurance Costs with Better Rental Rates

You shouldn’t have to choose between financial safety and a low price. A “cheap” daily rate often hides the true cost of the move. When you ask, do I need insurance for a rental truck, you must look at the total package. Protection plans are essential. They can also inflate your budget if you haven’t secured a competitive base rate first. Smart movers use a specific strategy. They find the lowest possible truck rental rate to make room for comprehensive insurance. This approach removes the stress of the “insurance upsell” because the cost is already covered by your savings elsewhere.

High-stakes logistics require clarity. Waiting until you are at the rental counter to decide on coverage is a mistake. The pressure is high. The jargon is thick. By comparing total costs ahead of time, you maintain control over your finances. You transform a confusing transaction into a simple, logical task. Efficiency is the goal. Transparency is the tool.

Finding the Best Base Rate with DityTruck

DityTruck acts as your smart assistant. It performs the heavy lifting by scanning top national brands instantly. It finds the lowest starting prices for your specific dates. In 2026, local rental base rates for large trucks typically range from $130 to $250 per day. Smaller in-town options often start between $19.95 and $39.95. These numbers don’t include mileage or protection. If you save $20 per day on the truck base rate by comparing options, that money effectively pays for your Damage Waiver. You get full protection without increasing your original moving budget. This level of transparency lets you see the full financial picture before you ever talk to a rental agent. It’s the shortest path between a problem and a cost-effective resolution.

Final Checklist: Booking with Confidence

Booking in advance through a comparison tool simplifies the insurance decision. You can review the protection options at your own pace. There is no pressure from a salesperson. Use the One Way Truck Rentals for Moving: 2026 Comparison Guide to see which providers offer the best value for your specific route. Once you’ve verified your personal insurance gaps as discussed in previous sections, you can select the right add-ons with total confidence.

Confirm your reservation and insurance selection online. Keep your digital receipt and your coverage verification notes handy. You are now ready for a friction-free move. Don’t gamble with your savings. Ready to move? Compare rental truck rates and book your move today at DityTruck.

Take Control of Your Moving Protection

Driving a massive box truck shouldn’t feel like a financial gamble. You now have the tools to answer the question, do I need insurance for a rental truck, with total certainty. Remember that standard auto policies and credit cards often leave you exposed because of weight limits and cargo exclusions. By following our five-step verification process, you can identify exactly where your personal coverage ends and where rental-specific protection needs to begin. Closing these gaps is the only way to ensure a friction-free moving day.

The smartest way to afford comprehensive coverage is to save on the vehicle itself. DityTruck simplifies this by letting you compare top national brands in seconds. You get transparent pricing with no hidden surprises, making it easy to see the full cost of your move upfront. Whether you are planning a local haul or a long-distance journey, we provide streamlined booking for every scenario. Find the best rates and book your rental truck now at DityTruck. You’ve done the research and verified the facts. Now, get behind the wheel with the confidence that you and your belongings are fully protected.

Frequently Asked Questions

Does my car insurance cover a 26-foot moving truck?

No, your personal car insurance will not cover a 26-foot truck. These large vehicles are classified as commercial-grade equipment. Most personal policies have a strict weight limit of 10,000 pounds. A 26-foot truck can reach a weight of 26,000 pounds when fully loaded. This massive size puts the vehicle well outside the boundaries of standard passenger car protection.

Does my credit card cover rental trucks for moving?

No, credit card rental benefits almost always exclude vehicles with a cargo box or a truck bed. These benefits are designed for standard cars, minivans, and SUVs. If the vehicle is intended for hauling freight, the coverage is void. You should never rely on your card when you ask, do I need insurance for a rental truck, because the fine print is very clear about these exclusions.

What happens if I hit a low bridge in a rental truck?

You will likely be held responsible for the full cost of the repairs. Most rental protection plans explicitly exclude overhead damage caused by low clearances. This is considered a preventable driver error. Even if you purchase a Damage Waiver, the company can still bill you for roof repairs. Always check the clearance height sticker on your dashboard before driving under any structure.

Is rental truck insurance legally required?

State law requires basic liability insurance, and the rental company usually provides the bare minimum. You aren’t legally forced to buy the extra damage waivers or supplemental policies. However, you are legally responsible for the full value of the truck. If you decline the coverage and cause an accident, the rental company will expect immediate payment for all damages and administrative fees.

What is a Loss of Use fee in truck rentals?

A Loss of Use fee covers the revenue a rental company loses while a truck is in the repair shop. If an accident takes a vehicle out of service for five days, you pay the daily rental rate for those five days. This charge is added to the actual cost of the repairs. A rental company’s damage waiver is often the only way to avoid this specific out-of-pocket expense.

Does insurance cover my furniture if the rental truck is stolen?

Standard damage waivers only protect the truck itself. To protect your belongings, you need specific Cargo Insurance or a homeowners policy with off-premises coverage. Many plans will deny your claim if the truck was left unlocked or if you didn’t use a high-quality padlock. Always confirm the specific theft requirements in your protection agreement before you start loading your furniture.

Can I buy rental truck insurance from a third party?

Yes, you can purchase transit insurance from specialized third-party providers. These policies can sometimes offer broader coverage for a lower daily price. However, they are often less convenient than the options offered at the rental counter. If an accident happens, you will likely have to pay the rental company first and then seek reimbursement from your third-party insurer later.

Is the Damage Waiver worth the extra cost?

Yes, it is the most reliable way to protect your personal savings. It turns a potential $40,000 disaster into a small, fixed daily expense. When you wonder, do I need insurance for a rental truck, consider the high cost of mechanical or body repairs. Paying for the waiver ensures you can return the keys and walk away without a massive bill after a single mistake.