Most personal auto insurance policies and credit card benefits exclude coverage for rental trucks due to their size and weight. It’s a sobering fact many drivers discover only after a minor scrape. If you’re wondering what happens if you damage a rental truck, the reality often involves high repair costs and unexpected administrative charges. Minor scratches alone can cost between $300 and $600 when billed by the rental company.

Moving is already a high-stakes task. You don’t need the added stress of confusing insurance jargon or hidden fees like loss of use charges that can cost up to $50 per day. We believe in total transparency. This guide provides a no-nonsense breakdown of the financial and legal consequences of rental truck damage. You will get a clear understanding of out-of-pocket limits and learn how to document pre-existing damage to avoid unfair bills. We’ll preview the coverage options that offer real protection so you can move with confidence.

Key Takeaways

- Prioritize safety and capture high-resolution photo evidence immediately after any incident.

- Understand what happens if you damage a rental truck when your personal insurance and credit cards provide zero coverage.

- Identify high-risk areas like overhead clearance and tires to avoid the most expensive repair bills.

- Prepare for hidden fees like loss of use and diminishment of value that drive up out-of-pocket costs.

- Shield yourself from liability by performing a rigorous pre-rental inspection with the agent present.

The Immediate Aftermath: Steps to Take After Damaging a Rental Truck

The sound of crunching metal or scraping fiberglass is a nightmare for any driver. If you find yourself in this situation, take a deep breath. Knowing exactly what happens if you damage a rental truck helps you stay in control of the situation. Your first priority is safety. Move the truck to a secure location away from traffic if it is still operable. Activate your hazard lights immediately. Check everyone involved for injuries; call emergency services if anyone needs medical attention. A calm, methodical approach prevents a stressful accident from becoming a financial disaster.

Once the scene is stable, start gathering evidence. You are your own best advocate in a liability dispute. Take high resolution photos and videos of the scene before moving the vehicle if possible. If other parties are involved, exchange contact details and insurance information. Collect names, phone numbers, and driver’s license numbers. Solid evidence prevents future disputes and ensures the facts speak for themselves. This documentation is the foundation of your defense against unfair claims.

Documenting the Scene Correctly

Effective documentation requires more than a few blurry snapshots. Start with wide shots that show the entire area. These photos provide context for how the accident occurred. Next, take close up shots of the specific damage. Capture the depth of dents or the length of scratches. Use a common object like a coin to show scale if the damage is minor. Detailed visuals eliminate guesswork during the repair estimate process.

Don’t forget the interior and the dashboard. Photograph the odometer and fuel gauge to establish the exact state of the truck at the time of the incident. Briefly note the environment in your phone’s notes app. Record the weather, lighting, and any road hazards. A quick video walkaround of the entire vehicle ensures you have proof of areas that were not damaged. This prevents the rental company from charging you for pre existing issues.

Reporting to the Rental Agency

Understanding what happens if you damage a rental truck is the first step toward a resolution. Contact the rental company immediately after securing the scene. Use their 24/7 roadside or claims line to report the incident. Never wait until you return the truck to disclose damage. Early reporting proves transparency and allows the company to guide you through their specific protocol. It also ensures that any necessary repairs or replacements are handled quickly.

Understand the difference between your points of contact. Roadside assistance helps with towing or mechanical failures. The claims department handles the financial liability and the actual repair process. If you purchased a Collision Damage Waiver, they will explain how it applies to your specific case. When you finally return the truck, you will need to complete a formal Damage Report form. Be honest and consistent with the information you provided over the phone. Clear communication stops hidden fees before they start.

Why Your Personal Car Insurance Probably Won’t Cover a Rental Truck

Assuming your personal auto insurance follows you into the cab of a box truck is a costly mistake. Most drivers think “full coverage” means exactly that. It doesn’t. Standard policies are written for cars, SUVs, and light pickups. When you step up to a rental truck, the rules change. Understanding what happens if you damage a rental truck starts with reading your policy’s fine print. You’ll likely find that size matters more than your driving record.

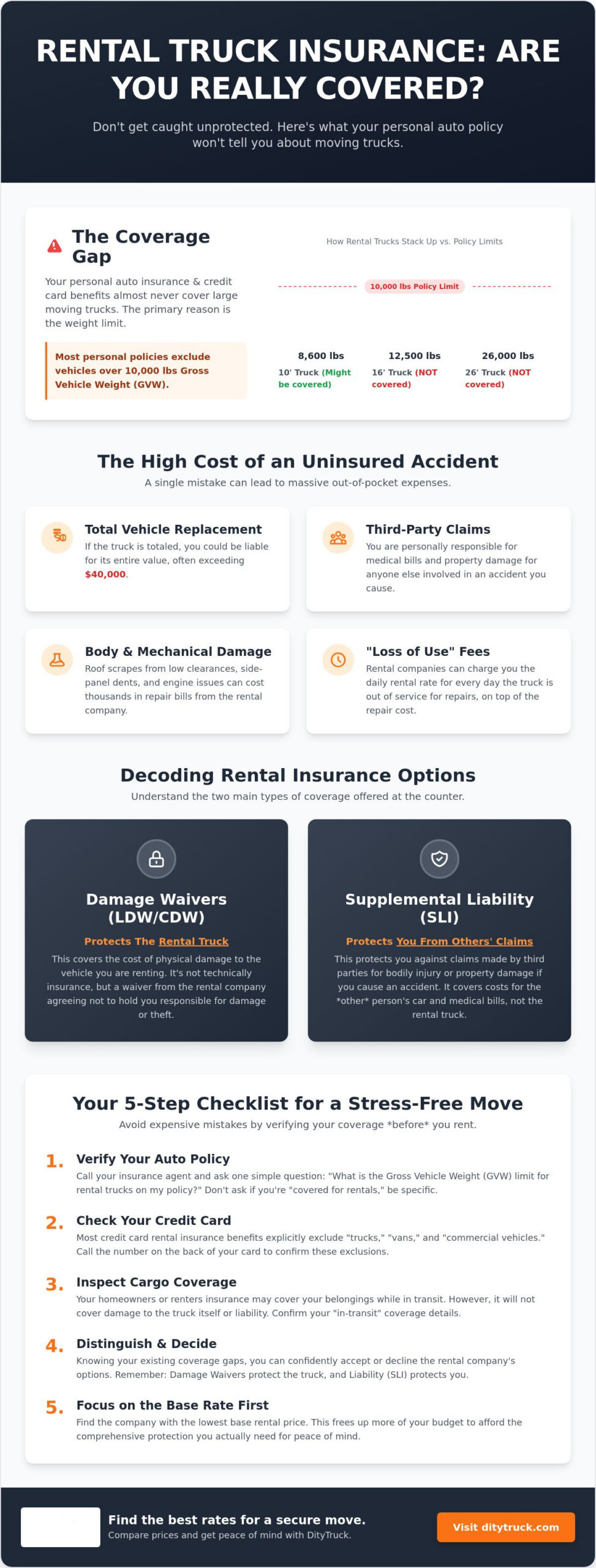

The 10,000-pound rule is the most common hurdle. Most personal insurance providers draw a hard line at this weight. If the truck exceeds this limit, your coverage vanishes. This leaves you personally responsible for every cent of repair costs. Additionally, if you’re moving for a new job or relocating a business, your policy may classify the trip as “business use.” This is a standard exclusion that can lead to a denied claim. You are suddenly exposed to thousands of dollars in liability with no safety net.

The Weight Limit Trap

Gross Vehicle Weight Rating, or GVWR, is the maximum operating weight of a vehicle. This figure includes the truck, the fuel, and all your cargo. A standard 26-foot moving truck can easily have a GVWR of 26,000 pounds. This is more than double the limit of most personal GEICO or State Farm policies. Even mid-sized 15-foot trucks often hover right at the 10,000-pound mark. If you’re unsure about the size you need, compare rental truck options before you book to ensure you stay within your coverage limits.

Credit Card Coverage Realities

Don’t rely on your gold or sapphire card to save the day. While many credit cards offer secondary rental insurance, they almost always exclude “trucks” and “cargo vans.” Their benefits guides specifically target passenger cars. Language like “vehicles with a cargo bed” or “commercial vehicles” is a red flag. These exclusions mean your card won’t pay a dime for a dented roof or a cracked windshield. Always call your bank’s benefits administrator to verify coverage for the specific class of vehicle you intend to rent.

Finally, consider the “Loss of Use” gap. This is a fee rental companies charge for the revenue lost while a truck is being repaired. Even if a miracle happens and your insurance covers the physical damage, they almost never pay for Loss of Use. You could be stuck paying the daily rental rate for a truck that is sitting in a body shop. This is exactly what happens if you damage a rental truck without the right supplemental protection. The costs stack up quickly while the vehicle is off the road.

The Most Common (and Costly) Types of Rental Truck Damage

Not all damage happens in a high speed collision. Most rental truck claims stem from simple errors in judgment. Understanding what happens if you damage a rental truck requires a look at the specific parts of the vehicle most likely to take a hit. From the roof to the tires, the costs vary wildly. Knowing these high risk areas helps you focus your attention where it matters most.

Overhead clearance strikes are the most expensive mistakes. Most drivers aren’t used to a 13 foot height. They clip bridges, gas station awnings, or low hanging branches. These impacts often result in catastrophic damage to the aluminum or fiberglass box. Because the damage is often structural, the repair bills are frequently the highest in the industry.

Curb strikes are another frequent issue. A heavy truck hitting a curb at the wrong angle can destroy a tire or bend a steel rim. Unlike a car, a truck blowout can damage the wheel well and the cargo floor. These repairs add up quickly. It’s easy to misjudge a turn in a vehicle with a long wheelbase, so take every corner wide.

Don’t forget the interior. Spills, stains, and cigarette smoke lead to heavy cleaning fees. If the odor is permanent, the company may charge you for a full interior detail or replacement of seat covers. Keeping the cab and cargo area clean is the simplest way to avoid these “soft” damage charges.

Then there are the minor dings. Most rental companies use the “quarter sized” rule. If a scratch is smaller than a quarter and doesn’t penetrate the paint, they usually let it slide. If it’s larger or deeper, expect a bill. Bumper scrapes alone can range from $400 to $1,200 depending on the material. This is a common part of what happens if you damage a rental truck, so watch your corners during tight turns.

The Danger of Low Clearances

Standard waivers frequently exclude the “box” or “roof” of the truck. This means even if you bought insurance, you might still be 100% liable for a roof strike. Replacing a single aluminum roof panel can cost thousands. The repair involves labor intensive riveting and sealing to ensure the box remains watertight. Avoid drive-thrus and parking garages entirely. Stick to truck approved routes to keep your roof intact.

Wear and Tear vs. Negligence

Normal wear and tear includes minor paint chips or worn floor mats. These are expected over the life of a commercial vehicle. Mechanical failures like a blown transmission or a faulty alternator are the company’s problem, provided you weren’t abusive. However, your protection ends where negligence begins. Driving on a flat tire instead of stopping immediately is a prime example. Negligence (like driving on a flat) voids most waivers. This turns a simple tire change into a full axle repair on your dime.

The Financial Fallout: Fees and Out-of-Pocket Expenses

The bill for an accident goes far beyond a body shop estimate. When people ask what happens if you damage a rental truck, they usually focus on the visible dent. The reality is a stack of line items that can double the final cost. These fees are designed to keep the rental company’s fleet profitable even when a vehicle is grounded. You are paying for the repair and the disruption to their business model.

Loss of Use is often the most surprising charge. This fee covers the revenue the company loses while the truck is in the shop. If a repair takes ten days, you pay for ten days of potential rentals. These charges typically range from $25 to $50 per day. This applies even if the company has other trucks available; they only need to prove the damaged truck could have been rented.

Diminishment of Value is another hidden cost. A truck that has been in a major accident is worth less on the resale market. Even with a perfect repair, the vehicle’s history report is permanently flagged. Companies often charge a fee to recover this lost equity. These charges frequently fall between $200 and $500. It is a standard industry practice to protect their long term assets.

Administrative fees and logistics costs add more weight to the bill. Expect a charge for the paperwork involved in your claim. Processing a damage report takes time and labor. Most companies bill between $50 and $150 just to open the file. If the truck isn’t drivable, you are also responsible for the tow. Storage fees at a yard can add hundreds of dollars before a technician even looks at the damage. This total package is the true answer to what happens if you damage a rental truck without adequate protection.

Understanding Loss of Use

Rental companies must justify their Loss of Use charges. They do this by showing their fleet utilization rates. If every other truck of that size was rented out during the repair period, the loss is clear. You can dispute these charges if the lot was full of idle vehicles. Ask for a fleet utilization report for the specific dates the truck was out of commission. Transparency is your best tool for lowering these secondary costs.

The Role of the Deductible

Your out of pocket limit depends entirely on your chosen coverage plan. Basic options like SafeMove often carry a $250 deductible for specific incidents like overhead damage. Premium plans might offer a $0 deductible for most accidental damage. Paying more upfront for a waiver often saves thousands in the long run. It is the difference between a small daily fee and a massive surprise bill. Compare rental truck booking options to find a plan that fits your risk tolerance and protects your budget.

How to Protect Yourself Before and During Your Rental

Prevention is the most effective way to manage your liability. You’ve seen the potential fees and the gaps in personal insurance coverage. Now, focus on proactive steps that keep your budget intact. By taking the right precautions, you can avoid the stress of wondering exactly what happens if you damage a rental truck during your move. Protection starts before you even turn the key.

Rushing through the pickup process is a common mistake. The lot is busy and you are in a hurry to start loading. Stop. A thorough inspection is your only defense against being billed for someone else’s accident. Walk the entire perimeter with the rental agent. Point out every scratch, no matter how small. If it isn’t on the contract, it didn’t exist before you arrived. This simple habit stops disputes before they begin.

Safe driving habits change with the vehicle size. Use the “Circle of Safety” before every single drive. This means walking around the truck to check for low hanging branches, tight corners, or hidden obstacles. It only takes thirty seconds. This routine prevents the most common causes of damage, like curb strikes and roof scrapes. It’s a small investment of time that provides massive peace of mind.

The Pre-Rental Inspection Checklist

Your inspection must be methodical. Use your phone to take high resolution photos of every panel. Focus on these high risk areas:

- The Roof: Look for scrapes or patches. Roof damage is rarely covered by standard waivers.

- The Tires: Check for sidewall bulges or low tread. A blowout can lead to a negligence claim.

- The Glass: Spot tiny chips in the windshield. These can spiderweb into large cracks during your trip.

- The Box Interior: Ensure the floor is clean and the tie downs are secure.

Documenting these details ensures you aren’t held responsible for previous wear. To find companies with the most transparent rental agreements, Compare Moving Truck Rental Rates and read the fine print on their damage policies before you sign.

Leveraging Comparison Tools

Transparency is the enemy of hidden fees. When you use a comparison tool, you see insurance options side-by-side. This prevents “insurance surprises” at the rental counter. You can evaluate the cost of a zero deductible plan against the potential out of pocket expenses. This clarity allows you to choose a protection level that matches your specific route and comfort level. You deserve a move that is simple, honest, and free of financial shocks.

Choosing the right provider is about more than just the daily rate. It’s about knowing what happens if you damage a rental truck and having a plan to handle it. DityTruck simplifies this process by highlighting the most reliable options in the industry. You get the facts you need to make a smart decision. Compare rental rates and protection plans on DityTruck today and take the friction out of your next move.

Drive with Total Confidence

You’ve done the research. You know that personal auto policies often stop at the 10,000 pound mark. You understand that “loss of use” fees can double a repair bill. Now that you know exactly what happens if you damage a rental truck, you can make a smarter choice at the counter. Knowledge is your best protection against hidden logistics costs. It allows you to focus on the move itself rather than potential liabilities.

Don’t leave your finances to chance. You need a partner that prioritizes honesty and speed. DityTruck offers a transparent booking process that shows you exactly what you are paying for before you sign. With national coverage across the US and real-time rate comparison, finding the right protection plan is simple. Find the best rental truck rates and protection plans on DityTruck to keep your move stress free. We strip away the complexity so you can stay in control.

Your next move should be about a fresh start, not a financial hurdle. Take the right precautions, document your vehicle, and drive with total peace of mind. You have the tools to handle the road ahead.

Frequently Asked Questions

Does my credit card cover damage to a 26-foot moving truck?

No, standard credit card rental insurance almost always excludes commercial sized vehicles and box trucks. Most benefits guides specifically list “trucks” or “vehicles with a cargo bed” as ineligible for coverage. You should call your bank to confirm, but assume you are personally liable for any damage to a large moving vehicle. This weight exclusion is a standard industry practice for secondary insurance providers.

What is a “Loss of Use” fee in a truck rental contract?

A Loss of Use fee is a charge for the revenue the rental company loses while a vehicle is grounded for repairs. If the truck is in the shop for five days, the company may bill you for five days of potential rental income. These fees often range from $25 to $50 per day. They apply even if the company has other trucks available on the lot during that time.

Will the rental company charge me for a small scratch on the bumper?

Rental companies typically follow the “quarter sized” rule for minor cosmetic damage. If a scratch is smaller than a coin and hasn’t penetrated the paint, it is often classified as normal wear and tear. However, deeper bumper scrapes or larger dents can result in repair bills ranging from $400 to $1,200. The cost depends on the material and the labor required for a professional fix.

What happens if I hit a low bridge with a rental truck?

Hitting a low bridge often results in catastrophic structural damage that is excluded from basic insurance waivers. You are likely responsible for the full cost of replacing the roof or the entire cargo box. Some premium plans include overhead damage protection with a $0 deductible. Basic plans may carry a $250 deductible for these specific incidents, so check your contract before you drive.

Can I be held liable if someone else hits my parked rental truck?

Yes, you are contractually responsible for the vehicle from the moment you sign the contract until the final return inspection. Even if you are not at fault, the rental company will look to you for payment. You must collect the other driver’s insurance information and file a police report immediately. This documentation helps the rental agency recover the costs from the responsible party instead of your pocket.

Is it worth buying the Damage Waiver (LDW) from the rental company?

Buying the waiver is generally worth the cost because personal auto policies rarely cover vehicles over 10,000 pounds. These waivers can reduce your financial responsibility to zero for most accidental damage. It is a small daily fee that prevents you from paying thousands out of pocket later. This is a primary factor in what happens if you damage a rental truck without a safety net.

What should I do if the rental company charges me for damage I didn’t cause?

Immediately dispute the charge using your pre-rental photos and the signed inspection report. Contact the company’s claims department and provide time-stamped evidence showing the damage existed before your rental period began. If the charge remains, you can escalate the issue through your credit card provider. Honest documentation is your best defense against administrative errors or unfair billing practices.

How long does a rental truck damage claim take to resolve?

Resolution times vary based on the extent of the damage and the speed of the repair shop. Most claims take between thirty and ninety days to fully process. This includes the time needed to estimate repairs, calculate loss of use fees, and coordinate with insurance providers. Understanding what happens if you damage a rental truck helps you prepare for this lengthy administrative process and stay organized.