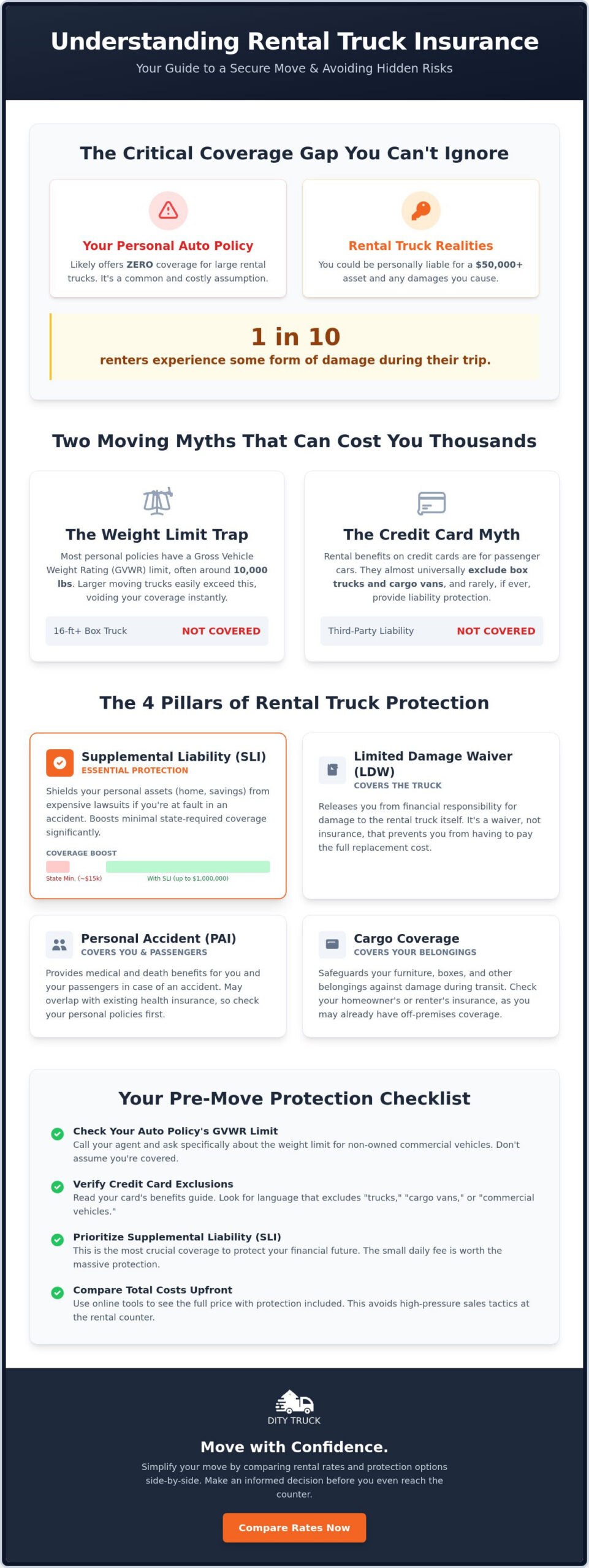

What if you found out your “full coverage” car insurance ends the moment you step into a 10,000-pound moving truck? Most personal policies stop where the heavy vehicle begins, potentially leaving you liable for a $50,000 asset. It’s a high-stakes risk, especially since 1 in 10 renters experience some form of damage during their trip. This is why having rental truck liability coverage explained clearly is vital before you reach the rental counter. You don’t want to make a split-second decision while a line of people waits behind you and an agent pushes expensive extras.

We know the pressure of moving day is already high. You shouldn’t have to decode an alphabet soup of SLI, LDW, and PAI while staring at a confusing contract. This guide strips away the complexity to show you exactly what those acronyms mean and where your current insurance falls short. We’ll help you identify which protection is essential and which is just a redundant expense. You’ll finish this article knowing exactly how to protect your move in 2026 without overpaying for things you don’t need.

Key Takeaways

- Most personal auto policies exclude vehicles used for cargo transport. Check your policy for the Gross Vehicle Weight Rating limit before you drive off the lot.

- Get rental truck liability coverage explained to understand why Supplemental Liability Insurance is your best defense against expensive third-party claims.

- Weigh the daily protection fee against the $50,000 replacement value of a modern box truck. It is a small price for total peace of mind.

- Use our pre-move checklist to verify coverage gaps with your credit card issuer. Most cards specifically exclude box trucks from their rental benefits.

- Compare rates across major providers to see the full price. Seeing the total cost upfront prevents high-pressure sales tactics at the rental counter.

Rental Truck Liability vs. Personal Auto Insurance

Liability coverage is your financial shield if you cause an accident. It pays for the other driver’s medical bills and vehicle repairs. Most drivers assume their personal auto policy handles this automatically. That is a dangerous assumption. Standard personal insurance usually excludes vehicles used for cargo transport or commercial purposes. Having rental truck liability coverage explained simply means understanding it is the bridge that fills the gap between your everyday car insurance and the specific risks of the rental contract.

Moving day involves heavy machinery. Your standard policy is written for sedans and SUVs, not 26-foot box trucks. If you cause an accident while driving a vehicle that your insurer considers “commercial grade,” you could be personally responsible for every cent of the damage. This includes:

- Third-party property damage to other cars or buildings.

- Medical expenses for injured parties.

- Legal fees if you are sued following a collision.

The Weight Limit Trap: Why GVWR Matters

Your personal policy likely has a hidden ceiling. It is called the Gross Vehicle Weight Rating (GVWR). Most policies stop covering vehicles once they exceed 10,000 pounds. A small cargo van might squeeze under this limit, but a 16-foot or 26-foot box truck will not. These larger trucks are heavy. They are harder to stop. They cause more damage. Insurance companies know this risk. They use weight limits to trigger automatic exclusions. Even if you are moving your own furniture, a “business use” or “commercial vehicle” clause can void your coverage because you are operating a heavy-duty truck.

Credit Card Coverage: The Biggest Moving Myth

Don’t rely on your gold or platinum card here. Most credit card benefits specifically exclude trucks, vans with seating for more than eight, and cargo vehicles. These perks are designed for passenger cars. If the vehicle is built for hauling freight, your card issuer will likely deny the claim. There is also a major difference between a Damage Waiver (DW) and true liability protection. Even if your card offers a collision waiver for the truck itself, it almost never provides liability coverage for the people you hit. You are left holding the bill for third-party damages while your card only covers the paint on the truck.

The 4 Main Types of Moving Truck Coverage

Understanding protection options is easier when you see the standard industry structure. Major providers like U-Haul, Budget, and Penske use different brand names for their packages. However, the actual coverage types remain remarkably consistent across the board. To get rental truck liability coverage explained properly, you must look at the four specific pillars that protect your finances, the vehicle, your health, and your belongings.

- Supplemental Liability Insurance (SLI): Protects you against lawsuits from third parties.

- Limited Damage Waiver (LDW): Relieves you of financial responsibility for the truck itself.

- Personal Accident Insurance (PAI): Provides medical and death benefits for you and your passengers.

- Cargo Coverage: Safeguards your furniture and boxes against specific types of transit damage.

Before you commit to a specific plan, it helps to compare rental rates and protection options side-by-side to ensure you aren’t paying for overlapping coverage.

Supplemental Liability Insurance (SLI) Deep Dive

SLI is often the most vital choice you will make at the counter. Every rental includes basic state-minimum liability, but these limits are often shockingly low. In some states, the minimum property damage coverage is only $15,000. If you hit a luxury SUV or a storefront, that amount disappears instantly. SLI boosts your protection to $1,000,000 in many 2026 rental contracts. This high limit shields your personal assets, like your home and savings, from being seized in a lawsuit. It is the primary way to get your rental truck liability coverage explained in terms of total asset protection.

LDW vs. CDW: What Are You Actually Waiving?

A Damage Waiver is not technically insurance. It is a contractual agreement where the rental company waives its right to collect damages from you. Without this, you are responsible for the full value of the truck. You may also face “loss of use” fees. These fees cover the daily revenue the company loses while the truck is being repaired. These costs can reach thousands of dollars before the first wrench even turns. High-standard government rental agreements often mandate these waivers because they eliminate the most common financial traps.

Be aware of the fine print. Most waivers exclude overhead damage. If you drive a 12-foot truck under a 10-foot bridge, the waiver is void. Tire damage and windshield chips are also frequent exclusions. Always inspect the roof and tires before leaving the lot to avoid being charged for pre-existing issues.

Calculating the Real Cost of Risk vs. Reward

Deciding on protection often comes down to a simple math problem. Daily rates for rental truck coverage typically range from $15 to $40 depending on the size of the vehicle. Compare this small daily fee to the average cost of a totaled box truck, which can easily exceed $50,000. For most movers, the peace of mind of knowing a single mistake won’t lead to bankruptcy far outweighs the marginal daily cost. It is about trading a small, known expense for protection against a catastrophic financial hit.

Your route also dictates your risk level. Driving a 26-foot truck through tight city maneuvers is vastly different from a short trip across a suburban town. Before you decline, get your rental truck liability coverage explained in the context of your specific path. Highway driving at high speeds increases the severity of potential accidents. Tight urban streets increase the frequency of minor scrapes. Both scenarios present unique financial dangers that standard personal policies rarely cover.

When You Can Safely Skip the Extra Coverage

There are rare moments when you can skip the counter add-ons without losing sleep. If you carry a high-limit personal umbrella policy, check if it specifically includes rental vehicles. Some high-end policies extend liability to trucks, though this is not the norm. Another exception is the small cargo van. If you are renting a van that falls under your personal auto policy weight limit, you might already be protected. Always verify this with a five-minute phone call to your agent. Reference this California Department of Insurance consumer alert to see why verbal confirmation is better than guessing. Never assume. A quick call ensures you don’t pay for redundant protection.

When Buying Coverage is Mandatory for Sanity

If you are a first-time truck driver, buy the coverage. The learning curve for wide turns and height clearances is steep. Most accidents happen because drivers forget the extra six feet of height or the massive blind spots. Cross-country moves also demand maximum protection. Long-distance trips involve higher risks of theft, extreme weather, and driver fatigue. Moving through high-traffic urban areas is equally risky. Tight parking, aggressive traffic, and low bridges are a recipe for property damage. In these high-stakes environments, the protection isn’t just about the money. It’s about ensuring a single clipped mirror or a low-hanging branch doesn’t derail your entire move. Getting rental truck liability coverage explained for these scenarios makes it clear that the protection is a tool for a stress-free transition.

Checklist: What to Ask Before You Sign

Moving day moves fast. You cannot afford to leave your financial safety to chance at the rental counter. Arriving prepared with a clear list of questions is the only way to avoid high-pressure sales tactics. Having rental truck liability coverage explained helps you spot gaps, but these four steps ensure you actually close them before you drive away.

- Step 1: Review your personal auto policy. Search specifically for a “Gross Vehicle Weight Rating” (GVWR) limit. If the truck weighs more than 10,000 lbs, your personal liability coverage likely ends at the driver’s seat.

- Step 2: Call your credit card company. Ask the representative if “cargo vehicles” or “box trucks” are excluded from their rental benefits. Do not accept a general “yes” for car rentals. Demand specifics on truck exclusions.

- Step 3: Compare coverage limits. Protection levels vary between providers. Use a truck rental comparison tool to view SLI limits and daily rates side-by-side before you book.

- Step 4: Perform a physical walk-around. Document every scratch, dent, and glass chip. If the damage isn’t on the contract, you may be held responsible for it later.

The Counter Talk: Dealing with Rental Agents

Agents often use “horror stories” about accidents to sell expensive add-ons. Stay firm. You have done the research and know your existing coverage gaps. Ask for the “Summary of Coverage” document before you pay. Read the fine print regarding deductibles. Some packages claim to offer “full protection” but still leave you with a $1,000 bill for accidental damage. Confirming the exact deductible amount prevents expensive surprises if you need to file a claim. If the agent cannot provide a clear summary, consider it a red flag.

Documenting Everything for Your Move

Your smartphone is your best defense against unfair damage claims. Take clear photos of all four sides of the truck. Do not forget the roof. Overhead damage is the most common exclusion in damage waivers. Getting rental truck liability coverage explained is only the first step; physical evidence is the second. Capture the interior cargo area and the fuel gauge. Keep the physical rental agreement and insurance summary in the glovebox at all times. The check-in process is just as critical as the check-out. When you return the truck, take another set of photos in the rental lot. This creates a time-stamped record. It prevents the company from charging you for damage that might happen after you leave the keys in the drop box.

Simplify Your Move with DityTruck

Finding the right truck shouldn’t feel like a second job. DityTruck helps you compare rates across major providers in one place. We focus on transparency. You see the total cost including potential fees before you commit. This clarity is essential. Once you have had the nuances of rental truck liability coverage explained, the next logical step is securing a vehicle that fits your budget and your protection needs. You can book your truck in minutes. Skip the stress of manual rate-hunting. We do the heavy lifting so you don’t have to. For more details on the process, check out our Moving Truck Rental: The Complete 2026 Comparison & Booking Guide.

Logistics can be a high-stakes task. We replace complexity with confident simplicity. Our platform acts as your savvy smart assistant. It performs the background research so you can focus on the physical move. You get a friction-free solution. No high-pressure sales tactics. No confusing jargon. Just a reliable tool that prioritizes your time. We value honesty and straightforwardness. Our goal is to provide the shortest, most logical path between your logistical problem and a successful resolution.

Comparing More Than Just Prices

Price is only part of the equation. DityTruck highlights critical differences in availability and truck sizes across the industry. Comparing Penske, Budget, and U-Haul side-by-side saves you more than just money; it saves you time and frustration. Every provider has different inventory levels. One might have the 26-foot truck you need while another is sold out. Our tool identifies these gaps instantly. You see the availability. You make the choice. If you are planning a long-distance trip, our One Way Truck Rentals for Moving: 2026 Comparison Guide provides a deeper look at how these companies stack up for interstate moves.

Ready to Book Your Truck?

Use our streamlined interface to secure your reservation today. There are no hidden hurdles or complicated forms. We provide a fast, efficient booking path for your next DIY move. You get the truck you want at a price that makes sense. Secure your peace of mind and get back to packing. Logistics simplified. Move completed. Compare Moving Truck Rates Now and start your journey with total confidence.

Take Control of Your Moving Day Protection

You now have the tools to avoid the most common financial traps of a DIY move. Remember that your personal auto policy likely stops at the 10,000-pound mark. Verifying your credit card exclusions and documenting the truck’s condition are your best defenses against unexpected fees. With rental truck liability coverage explained, you can now approach the rental counter with total confidence. You won’t be swayed by high-pressure tactics or confusing insurance acronyms. You know exactly what you need to protect your assets and your belongings.

DityTruck makes the next step simple and efficient. We provide real-time rates from top national providers and transparent pricing with no hidden fees. You can also access our expert moving resources for 2026 to stay ahead of every logistical hurdle. Compare Moving Truck Rental Rates and Book Your Move Today to secure your vehicle in minutes. Your move should be about new beginnings, not insurance headaches. Take the shortest path to a successful transition and start your journey with peace of mind today.

Frequently Asked Questions

Does my regular car insurance cover a rental moving truck?

Most personal auto insurance policies do not cover rental moving trucks. Coverage usually ends when a vehicle exceeds a specific weight limit, often 10,000 pounds. Since most box trucks surpass this limit, your insurer will likely deny any claims. Always call your agent to confirm if your specific policy includes an exception for DIY moves before you decline the rental company’s offer.

What happens if I hit a bridge with a rental truck?

You are typically responsible for the full cost of repairs if you hit a bridge. Most Damage Waivers and Limited Damage Waivers specifically exclude overhead damage. This means even if you bought the premium protection package, hitting a low-clearance obstacle remains your personal financial burden. Always check the height clearance decal inside the cab before you start driving.

Is Supplemental Liability Insurance (SLI) worth it for a one-day move?

Yes, Supplemental Liability Insurance is worth the cost even for short trips. A single accident can cause property damage or medical bills that far exceed the basic state-minimum liability provided by the rental company. Having rental truck liability coverage explained in terms of risk shows that a small daily fee is a smart way to protect your personal savings from a massive lawsuit.

Can I use my business insurance for a personal moving truck rental?

Business insurance rarely covers a personal move unless you have a specific Hired and Non-Owned Auto endorsement that allows for personal use. If the rental agreement is in your individual name rather than the business name, the commercial policy will likely not apply. Check with your commercial broker to see if your work policy extends to a household move before you skip the counter coverage.

Does U-Haul insurance cover my furniture if there is an accident?

U-Haul insurance only covers your furniture if you purchase a package that includes Cargo Protection, such as SafeMove or SafeMove Plus. Basic liability only protects you against damage you cause to others. Cargo coverage protects your belongings against fire, windstorm, or collision. It does not cover damage caused by poor packing or items shifting during the drive.

What is the difference between LDW and CDW in truck rentals?

There is virtually no difference between a Limited Damage Waiver (LDW) and a Collision Damage Waiver (CDW) in the truck rental industry. Both are contractual agreements where the rental company waives its right to charge you for damage to the vehicle. They are not insurance products. Instead, they are a release of financial liability for the truck itself while it is in your possession.

Will my credit card cover a 10-foot cargo van rental?

Most credit cards will not cover a 10-foot cargo van. Card issuers typically exclude cargo vehicles, trucks, and open-bed vehicles from their rental insurance perks. Even if the van feels like a large SUV, the cargo designation on the registration usually triggers a coverage exclusion. Call your card issuer to ask specifically about cargo van exclusions to avoid a gap in protection.

What should I do if I have an accident in a rental truck?

First, ensure everyone is safe and call 911 to file a police report. Take photos of all vehicles involved, the surrounding scene, and the rental truck’s damage from multiple angles. Contact the rental company’s emergency roadside assistance line immediately to report the incident. Understanding rental truck liability coverage explained helps you stay calm because you will know exactly which protection products you purchased at the start of your trip.