Your credit card’s rental protection is likely useless for your move. Most personal auto policies and standard credit cards exclude vehicles over a certain weight, leaving you fully responsible for a massive truck. Understanding the moving truck rental damage waiver cost helps you avoid expensive surprises at the rental counter. It’s about knowing exactly who pays if you scrape a low-hanging branch or clip a curb in an unfamiliar, heavy vehicle.

It’s stressful to navigate a large truck through tight streets while worrying about potential repair bills. You want a smooth transition without the fear of being scammed or hit with hidden fees. This guide helps you master the complexities of rental protection so you can decide if a waiver is a smart investment for your 2026 move. We will break down exactly what these waivers cover, compare your protection options, and give you the clarity needed to book your truck with total confidence.

Key Takeaways

- Learn why a damage waiver is a legal contract amendment rather than a traditional insurance policy.

- Discover why standard protection often excludes overhead damage and how to avoid these expensive coverage gaps.

- Check your existing auto insurance and credit card limits to confirm if they actually cover large rental vehicles.

- Use a comparison tool to analyze the moving truck rental damage waiver cost alongside the base rental fee for an accurate total price.

What is a Moving Truck Rental Damage Waiver?

A damage waiver is not insurance. This is the most common misconception in the logistics industry. When you analyze the moving truck rental damage waiver cost, you are looking at a contractual agreement rather than a standard policy. The rental company essentially agrees to “waive” their legal right to collect repair costs from you if the vehicle is damaged during your move. Without this waiver, you remain financially responsible for every scratch, dent, or mechanical failure that occurs while the keys are in your hand.

The primary objective here is to prevent a “Total Loss” scenario. A modern 26-foot moving truck represents a significant capital investment, often valued at tens of thousands of dollars. If a major accident occurs, the rental provider would typically seek the full replacement value from the renter. By opting into a waiver, you shift this massive financial liability from your personal bank account back to the rental company. It provides a ceiling on your potential losses; it ensures a single mistake on the road doesn’t lead to long-term financial ruin.

LDW vs. CDW: Understanding the Terms

You will likely see two acronyms at the rental counter: LDW and CDW. A Collision Damage Waiver (CDW) is the narrower option. It generally covers the truck if it is involved in a traffic accident or hits a stationary object. A Loss Damage Waiver (LDW) is more comprehensive. It includes collision protection but also covers the “loss” of the vehicle due to theft, fire, or vandalism. Identifying which term your provider uses is critical for your peace of mind. If you are parking the truck in an unsecured area overnight, an LDW is the superior choice because it accounts for more than just your driving skills.

Why Rental Protection is Unique

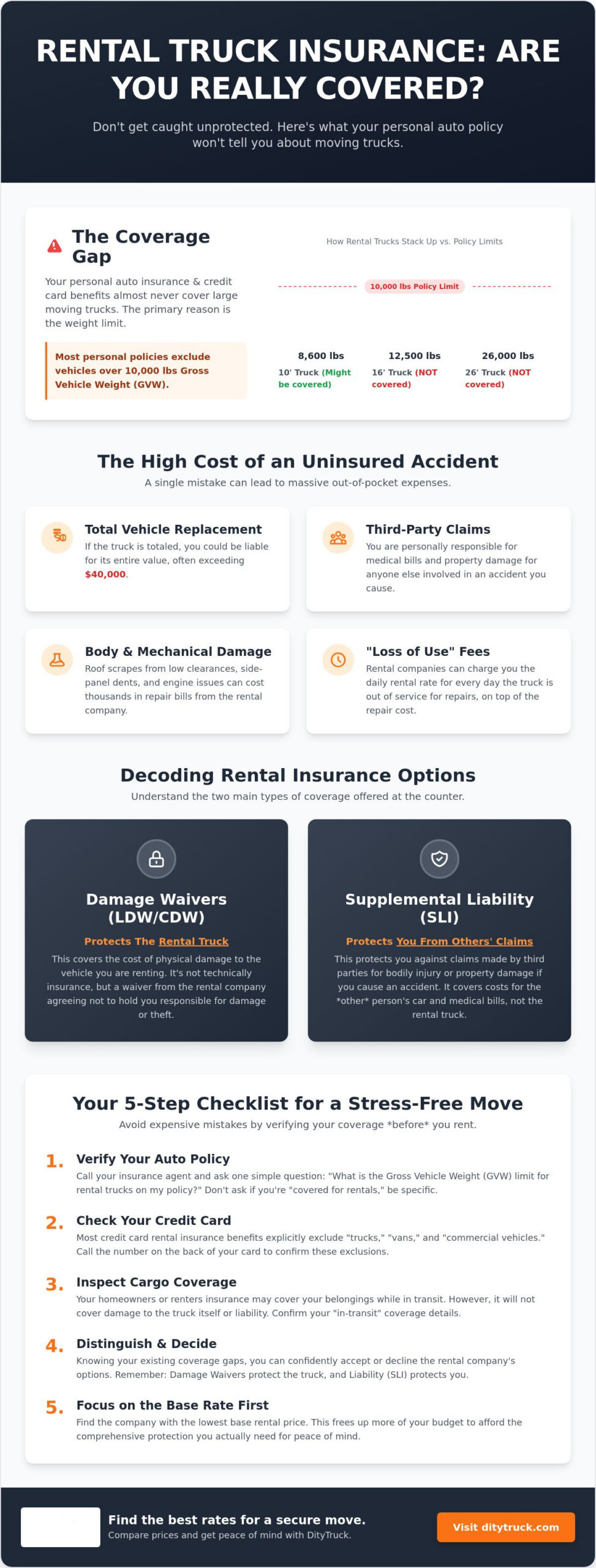

Moving truck protection differs significantly from the coverage you get when renting a standard sedan. The main factor is vehicle weight. Most personal auto insurance policies and credit card benefits specifically exclude vehicles over a certain Gross Vehicle Weight Rating (GVWR). Because moving trucks are heavy and have a high center of gravity, they are classified differently by underwriters. A damage waiver is a contractual transfer of risk. This unique legal status is why the What is a Damage Waiver? question is so common; it fills a specific gap that your daily insurance simply cannot reach.

Understanding the moving truck rental damage waiver cost involves recognizing that you are paying for the rental company’s permission to walk away from a damaged vehicle. It is a simple, effective way to strip away the complexity of high-stakes logistics. You aren’t just buying “coverage”. You are buying a guarantee that the rental company will not pursue you for the cost of a new truck if the unthinkable happens on the highway.

Comparing Damage Waiver Tiers and Protection Levels

Most rental companies present protection as a tiered system. You aren’t just choosing “yes” or “no”. You are selecting a level of financial immunity. The moving truck rental damage waiver cost varies significantly based on the vehicle size and your trip type. A small cargo van usually carries a lower daily rate than a 26-foot box truck. This reflects the increased risk and repair costs associated with a larger vehicle. It is a simple calculation of scale.

Duration and distance also play a role in the final price. For local moves, you might pay a flat daily fee. Long-distance, one-way trips often bundle the protection into the total reservation price. It’s smart to compare total reservation costs across different providers to see how these tiered fees stack up against each other. Identifying the right balance between cost and coverage is the fastest way to a stress-free move.

Standard Coverage Components

Basic tiers usually focus on the hardware. Physical damage protection covers the truck body and engine components. If you dent the side panel, the waiver handles it. Many premium bundles add cargo coverage and medical protection. Cargo coverage protects your belongings during a transit accident, though it often excludes high-value items like jewelry or electronics. Medical and life coverage provides a safety net for the driver and passengers. These bundles align with federal moving regulations designed to protect consumers during interstate relocations.

Liability Protection (SLI)

A standard damage waiver only protects the rental truck. It does not cover the other person’s car or their medical bills if you are at fault. This is a critical gap that many renters overlook. Supplemental Liability Insurance (SLI) fills this void. While every rental includes some state-mandated liability, these limits are often extremely low. SLI can provide up to $1,000,000 in additional coverage. This is especially important for long-distance moves where you spend more time in high-traffic areas and unfamiliar territory.

Choosing a tier requires balancing your risk tolerance with your budget. The moving truck rental damage waiver cost is an investment in your peace of mind. It ensures that a single mistake doesn’t turn into a liability lawsuit. Review each tier carefully before signing. Look for the specific dollar limits on cargo and liability to ensure they meet your needs. Clarity at the start prevents a financial disaster at the end.

The Fine Print: Common Exclusions and Coverage Gaps

Even after paying the moving truck rental damage waiver cost, you aren’t invincible. Many renters assume a waiver is a blanket shield against any bill. This is a dangerous mistake. Most standard agreements contain specific exclusions that can leave you on the hook for thousands of dollars. One of the most common pitfalls is the “authorized driver” rule. If you let a friend take the wheel to give yourself a break, you have likely voided your protection entirely. Only the individuals listed on the rental contract are covered. If an unlisted driver has an accident, the waiver is useless.

Tire and glass damage are other frequent gaps. Despite being the most common types of minor repairs, basic waivers often ignore them. If you hit a pothole and blow a tire or a rock cracks the windshield, the rental company may still charge you. When calculating the moving truck rental damage waiver cost, check if these items require a separate “roadside” or “premium” add-on. Skipping this detail could result in a 300 dollar bill for a single tire replacement at the end of your trip.

Why Overhead Damage is the #1 Risk

Driving a box truck is nothing like driving an SUV. The most expensive accidents often involve the roof. Most drivers aren’t used to checking height clearances for bridges, drive-thrus, or low-hanging tree branches. Because this damage is almost always considered preventable, rental companies typically exclude it from standard waivers. If you peel back the roof of a 26-foot truck on a low bridge, you are paying for the full repair out of pocket. To avoid this, look for “Premium” or “Plus” tiers. These higher-level packages are often the only way to get true overhead protection. Always verify the height of your truck, which is usually printed on a sticker inside the cab, before you start your engine.

Negligence and Policy Voids

Certain actions will cancel your waiver immediately. Using the wrong fuel is a classic example. Putting gasoline in a diesel engine causes catastrophic mechanical damage that no basic waiver will cover. Similarly, taking the truck off-road or using it for “reckless” purposes voids the agreement. A waiver is only valid if the contract terms are strictly followed. If an accident does occur, a police report is usually mandatory. Without official documentation from law enforcement, the rental company can reject your waiver claim and hold you personally liable for the full cost of the vehicle. Documentation is your best defense against unexpected charges.

How to Decide if the Damage Waiver Cost is Worth It

Deciding on protection requires a logical audit of your existing safety nets. You need to know exactly where your current coverage ends. The moving truck rental damage waiver cost is only worth it if you are currently exposed to financial risk. Most people are. Start by looking at your current assets and liabilities. It’s the only way to make a factual decision.

The Auto Insurance Myth

Don’t assume your personal policy has your back. Most standard auto insurance policies stop covering vehicles once they exceed 10,000 lbs Gross Vehicle Weight Rating (GVWR). A medium-sized 16-foot moving truck often hits this limit. Ask your insurance agent specifically about non-owned, non-commercial vehicles over five tons. Even if they say yes, consider the long-term impact. Filing a claim for a rental accident on your personal policy will likely raise your premiums for years. It’s a high price for a one-time event.

Credit Card Coverage Realities

Your gold or platinum card probably won’t help here. Most credit card agreements contain a specific Box Truck Exclusion. They are designed for passenger cars. They are not built for logistics. If you rely on card benefits, you might find yourself facing a massive deductible. Many cards offer only secondary coverage. This requires you to exhaust all other insurance options first. It creates a bureaucratic nightmare during an already stressful move. For a deeper look at booking logistics, check out our Moving Truck Rental: The Complete 2026 Comparison & Booking Guide.

Consider the replacement value of the equipment. You are operating a machine worth upwards of 50,000 dollars. Paying a small daily fee to walk away from that liability is a high-impact decision. Evaluate the complexity of your route. Are you driving through heavy city traffic? Is there a chance of severe weather? High-traffic environments and poor visibility significantly increase the likelihood of a scrape or collision. A single dent can cost more than your entire rental.

The moving truck rental damage waiver cost is a small price for total financial clarity. It replaces anxiety with a fixed, manageable expense. Before you sign your next contract, compare rental options and protection plans to find the most efficient path for your budget. Stripping away the risk allows you to focus on the move itself.

Compare Total Costs with DityTruck

DityTruck strips away the confusion of fragmented pricing. You shouldn’t have to visit several different websites just to understand the moving truck rental damage waiver cost. We aggregate the data so you can see the base rate, mileage, and protection fees in a single dashboard. This transparency ensures you aren’t hit with unexpected environmental fees, which typically range from 1 to 15 dollars; it also helps you account for mileage charges that often fall between 0.59 and 1.39 per mile. Having this data upfront changes how you book.

Transparency in Moving Logistics

Seeing all your options in one place prevents overpaying. Some providers offer a low base rate but inflate their protection fees to compensate. Others include a basic waiver in the initial quote, making them look more expensive at first glance. DityTruck helps you find the best base rate to offset your protection expenses. Booking early is your best strategy for a cost-effective move. Since 42 percent of annual rentals happen between June and August, demand drives prices up quickly. Lock in your rate now. Secure the most efficient path between your old home and your new one.

Your Next Steps for a Stress-Free Move

Your final checklist is the key to a smooth pickup. Before you hit the reserve button, confirm the total price includes all supplemental coverage. When you arrive at the counter, you’ll be prepared for the insurance pitch. You already know your personal auto insurance limits and the rental company’s specific exclusions. You are in control of the transaction. No last-minute pressure. No confusion. Just a clear path forward.

- Review the total cost including environmental and mileage fees.

- Estimate your fuel budget based on current diesel prices of approximately 4.15 per gallon.

- Confirm that all drivers are officially listed on the rental contract.

- Document the truck’s condition with photos before leaving the lot.

Compare Moving Truck Rental Rates in One Simple Step to start your move with total financial clarity.

Secure Your Move with Total Clarity

Managing your logistics shouldn’t involve financial gambling. You now understand that a damage waiver is a contractual shield rather than a typical insurance policy. It protects you from the total loss scenarios that standard auto policies often ignore due to vehicle weight limits. By evaluating the moving truck rental damage waiver cost against the high replacement value of the equipment, the smart choice becomes clear. You are paying for the right to walk away from a damaged vehicle without a catastrophic bill.

DityTruck simplifies this final step. Our platform allows you to compare top-rated national rental providers side-by-side in a single view. You will see the total cost upfront with no hidden fees, helping you avoid last-minute surprises at the counter. We are trusted by thousands of DIY movers annually to provide a friction-free booking experience. Find the best moving truck rates and protection today. Take control of your relocation and start your journey with the confidence you deserve.

Frequently Asked Questions

Is a moving truck damage waiver mandatory by law?

No, a damage waiver is not a legal requirement. It’s a voluntary contract amendment that limits your financial liability. While you can decline it, you remain 100 percent responsible for any damage to the vehicle during your rental period. Most renters choose it to avoid massive out of pocket expenses for a machine they don’t own.

Does my personal car insurance cover a 26-foot box truck?

Most personal policies exclude vehicles over 10,000 pounds. A 26-foot truck far exceeds this weight class. You’ll likely find that your standard coverage stops at passenger cars and small SUVs. Check your policy for gross vehicle weight exclusions before assuming you’re safe on the road. It’s a critical gap that leaves most DIY movers exposed.

What is the difference between SafeMove and SafeMove Plus?

SafeMove covers the truck, your cargo, and medical costs; SafeMove Plus adds one million dollars in Supplemental Liability Insurance. In 2026, basic Safemove starts around 14 dollars while the Plus version starts at 28 dollars. The extra cost is a small price for protection against lawsuits from other drivers. This significantly impacts your total moving truck rental damage waiver cost.

Does a credit card cover damage to a rental moving truck?

Credit cards almost never cover large moving trucks. Most cardholder agreements specifically exclude box trucks or vehicles designed for commercial use. Even premium cards that offer rental car protection usually have weight and size limits that disqualify moving equipment. Don’t rely on your plastic for this high stakes task.

What happens if I decline the waiver and have an accident?

You become personally responsible for the full repair costs and the rental company’s lost revenue. This includes loss of use fees while the truck is in the shop. If the truck is totaled, you owe the full replacement value. This can result in a bill for tens of thousands of dollars that you must pay out of pocket.

Can I buy third-party rental truck insurance instead of the company waiver?

Third-party options are extremely limited for heavy trucks. Most popular third-party rental insurers focus exclusively on passenger cars. If you find a policy, ensure it explicitly mentions the weight class of your truck. Buying directly from the rental counter is usually the most efficient way to secure valid protection without hidden hurdles.

Does the damage waiver cover my furniture and boxes?

A standard waiver only covers the truck, but many bundles include cargo protection. These policies often cover up to 25,000 dollars in damage to your belongings during an accident or fire. Keep in mind that high-value items like jewelry and televisions are frequently excluded from these basic cargo protections. Read the exclusions carefully before you load.

Does the damage waiver cover towing a car behind the truck?

Protection for a towed vehicle is usually available if you rent the trailer from the same company. The waiver must specifically list the towing equipment to remain valid. If you use your own trailer or tow dolly, the rental company’s waiver won’t cover damage to your car or the setup. Understanding these details helps you manage the moving truck rental damage waiver cost effectively.